Conventional mortgages are the most popular form of home financing for buyers in the United States. However, it may not always be clear how these loans differ from other loans, such as those provided by government agencies. To help you gain a better understanding of conventional loan basics, here is a quick guide with further information:

When obtaining conventional financing, your lender will examine your financial situation. The loan officer may request information including your credit score, income statements and debt to income ratios.

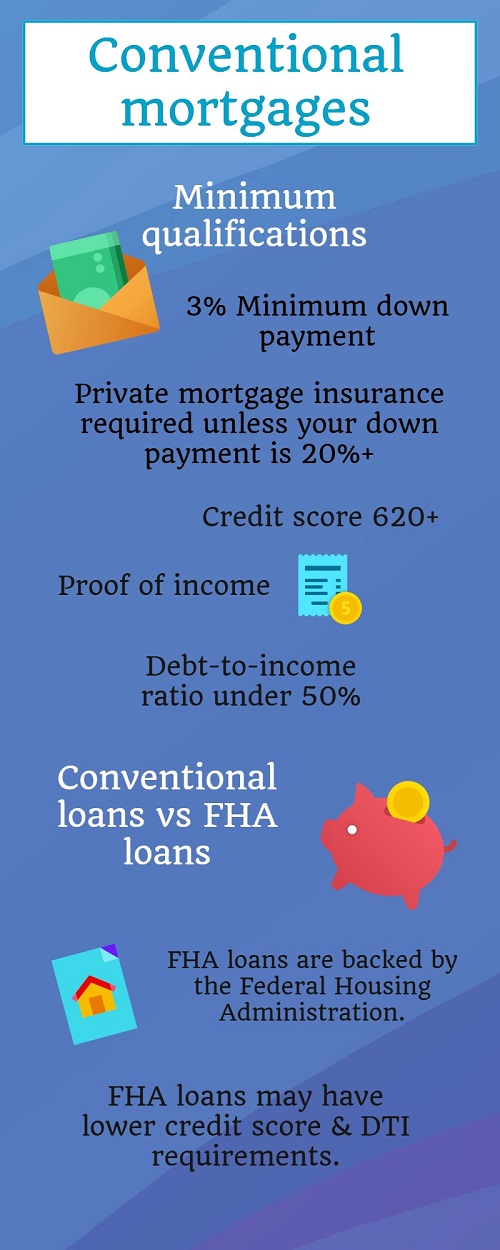

A down payment is required for conventional loans. Each lender has different minimum requirements, but the larger the down payment, the less money you’ll have to pay back over time.

Many believe a 20% down payment is required for conventional loans, but the minimum requirement is typically much lower. You can find mortgages with minimum down payment requirements anywhere from 3% to 20% of the overall purchase price.

Your choice of down payment amount can affect the terms of your mortgage, like interest rate or the need for private mortgage insurance.

Government-backed home loans have specific features to suit some homebuyers.

The Federal Housing Administration (FHA) is a government institution offering home loans for buyers who meet certain qualifications. Government-backed loans have advantages for those with bad credit or other financial roadblocks, but require other qualifications for approval.

Conventional mortgages tend to have higher interest rates than FHA loans, although these loans typically require borrowers to pay mortgage-insurance premiums.

Interest rates charged on a conventional mortgage vary by several factors, including the term and amount borrowed. However, interest rates are also subject to change every year based on the overall economy. Many buyers choose to wait for a period when interest rates are lower to apply for a mortgage, regardless of the loan type.

Ultimately, your choice of loan will depend on your personal circumstances. The more you know about different types of mortgage, the better equipped you’ll be for your journey into thefinancial real estate marketplace.

Kimberly Kelly decided to get her real estate license when she moved to South Orange with her family and fell in love with the classic, period homes of the area. Having worked in the city for many years for LexisNexis, Kim understands the appeal of an easy commute to NYC. That’s why she specializes in towns along the Mid-Town Direct train line, offering welcoming communities, good schools, and space to grow.

Very active in her children’s school PTA, Kim knows firsthand how important a school system is to parents looking to make the move to the ‘burbs. She volunteers with fairs, fundraising, and other activities that bolster support for education. Kim also believes involvement in the greater community enriches us all and has sat on various boards & associations throughout the years.

Kim Kelly has lived many places throughout her life, from Pennsylvania to Oregon, but has found New Jersey to be the ideal place to raise her family and put down roots. She loves nothing more than helping others discover their special place as well. Kim’s extensive knowledge of the area, combined with her sense of community, offers clients a personalized guide to finding the right house - and town - to call home.